Corporate dissolution is one of the crucial legal processes that enterprises must thoroughly understand when intending to terminate their business operations. A proper understanding and full compliance with dissolution procedures not only assist enterprises in ending their operations legally and avoiding the accrual of tax obligations or legal disputes, but also safeguard the rights and interests of owners and relevant stakeholders. Unlike bankruptcy procedures—which are implemented when an enterprise is insolvent and must be conducted through Court proceedings—corporate dissolution is carried out when the enterprise remains capable of ensuring the full settlement of all debts and asset obligations, and is not involved in any ongoing dispute resolution at a Court or Arbitration. Notably, the termination of operations through dissolution does not result in restrictions or prohibitions on holding management positions or conducting certain business activities for the enterprise owners and managers, as is the case under bankruptcy procedures.

According to statistics from the National Statistics Office, General Statistics Office – Ministry of Finance in the Report on the Socio-Economic Situation for April and the first four months of 2026: in April, there were nearly 20,400 newly established enterprises nationwide, more than 5,300 enterprises suspended operations awaiting dissolution procedures, and over 3,400 enterprises completed dissolution procedures[1]. Currently, corporate dissolution procedures in Vietnam are governed by the Law on Enterprises No. 59/2020/QH14 dated 17 June 2020 as amended and supplemented by the Law on Amendment to Law on Enterprises No. 76/2025/QH15 dated 17 June 2025 (“Law on Enterprises”), Decree No. 168/2025/ND-CP dated 30 June 2025 of the Government on business registration (“Decree 168”), the Law on Tax Administration No. 38/2019/QH14 dated 13 June 2019 (“Law on Tax Administration”), and Circular No. 86/2024/TT-BTC dated 23 December 2024 of the Ministry of Finance providing for tax registration (“Circular 86”).

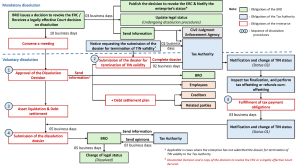

Diagram of basic steps in the corporate dissolution process

- Cases of corporate dissolution

The causes leading to corporate dissolution are diverse, but they are fundamentally categorized into two main cases:

1.1. Voluntary dissolution: This depends on the subjective will of the enterprise owner and is decided through a resolution or decision on dissolution by the owner of a sole proprietorship (for sole proprietorships); the company owner (for single-member limited liability companies); the Board of Members (for limited liability companies with two or more members and partnerships); or the resolution of the General Meeting of Shareholders (for joint stock companies) (hereinafter collectively referred to as the “Dissolution Decision”).

1.2. Mandatory dissolution: This does not depend on the subjective will of the enterprise owner but is carried out at the request of competent State authorities. It usually arises from violations committed by the enterprise or when the enterprise no longer meets the conditions to maintain business operations as prescribed by law, specifically including the following cases:

a. The expiration of the term of operation as stated in the company charter without a decision for extension;

b. The company fails to maintain the minimum number of members or shareholders as prescribed by law for a period of 6 consecutive months without performing procedures for conversion of the enterprise type;

c. The enterprise has its Enterprise Registration Certificate (“ERC”) revoked.

Specifically, the cases in which an enterprise shall have its ERC revoked include:

- The contents declared in the enterprise registration dossier are fraudulent;

- The enterprise was established by persons who are prohibited from establishing an enterprise under the law;

- The enterprise ceases business operations for 1 year without notifying the business registration office (“BRO”) and the tax authority (“Tax Authority”);

- The enterprise fails to submit reports as requested by the BRO within 6 months from the deadline for submitting reports or upon written request;

- Other cases as decided by the Court or upon the request of competent authorities as prescribed by law.

- Process and and procedures for corporate dissolution

2.1. Step 1: Approval of the Dissolution Decision

At this step, enterprises should take note of the following contents:

a. Timing for approving the Dissolution Decision:

For voluntary dissolution: The enterprise organizes a meeting to approve the Dissolution Decision according to its own scheduled plan.

For mandatory dissolution: The enterprise must convene a meeting to approve the Dissolution Decision within 10 days from the date of receipt of the decision to revoke the ERC or a legally effective Court’s decision.

b. Contents of the Dissolution Decision: This includes primary contents such as: the reasons for dissolution; the timeline and procedures for the liquidation of contracts and settlement of the enterprise’s debts; and the plan for handling obligations arising from labor contracts.

c. Activities strictly prohibited for the enterprise and enterprise managers from the issuance of the Dissolution Decision: (i) Concealing or dispersing assets; (ii) Waiving or reducing the right to debt recovery; (iii) Converting unsecured debts into debts secured by the enterprise’s assets; (iv) Entering into new contracts, except for the purpose of performing the corporate dissolution; (v) Pledging, mortgaging, donating, or leasing asset; (vi) Terminating the performance of effective contracts; and (vii) Raising capital in any form. Depending on the nature and severity of the violation, enterprise managers may be subject to administrative penalties or criminal prosecution; if damages are caused, compensation must be paid [2].

2.2. Step 2: Notification of the Dissolution Decision and fulfillment of procedures for termination of tax identification number (“TIN”) validity

a. Notification of the Dissolution Decision

For voluntary dissolution: Within 7 working days from the date of approval of the Dissolution Decision, the enterprise must send the Dissolution Decision, meeting minutes, and debt settlement plan (if any) to the BRO, the Tax Authority (pursuant to the procedures for termination of TIN validity below), and employees within the enterprise. The Dissolution Decision must be posted on the national business registration portal (“NBRP”) and publicly displayed at the headquarters, branches, and representative offices of the enterprise.

For mandatory dissolution: After approving the Dissolution Decision, the enterprise must send the Dissolution Decision and a copy of the decision to revoke the ERC or a legally effective Court decision to the BRO, the Tax Authority (pursuant to the procedures for termination of TIN validity below), and employees, and must publicly display it at the headquarters, branches, and representative offices of the enterprise. In cases where the law requires newspaper publication, the Dissolution Decision must be published in at least 1 printed or electronic newspaper for 3 consecutive issues. Where the enterprise still has outstanding financial obligations, it must simultaneously send the Dissolution Decision and the debt settlement plan to creditors and persons with related rights and obligations. The notice must include the name and address of the creditor; the debt amount, the deadline, location, and method of payment; and the procedures and timeline for resolving creditor complaints.

b. Fulfillment of procedures for termination of TIN validity

The enterprise must perform procedures to terminate its TIN validity at the directly managing tax authority in both cases of voluntary and mandatory dissolution.

Prior to submitting the application for termination of TIN validity, the enterprise must complete: (i) obligations regarding invoices in accordance with the law on invoices; (ii) obligations to submit tax declaration dossiers, pay taxes, and settle overpaid tax amounts or non-deducted value-added tax (if any) as prescribed, including obligations under TINs for payments made on behalf of others (if any).

The dossier for the termination of TIN validity consists of [3]:

- An application for termination of TIN validity using Form No. 24/DK-TCT issued with Circular 86.

- A copy of the Dissolution Decision.

Note: In cases where the enterprise has dependent units, all such units must complete the procedures for termination of their respective TIN validity before the enterprise’s TIN validity can be terminated [4].

Upon receipt of the enterprise’s dossier for termination of TIN validity, the Tax Authority shall perform the following tasks[5]:

- Issue a Notice of the enterprise’s suspension of operations and ongoing procedures for termination of TIN validity (Form No. 17/TB-DKT issued with Circular 86) to the enterprise within 2 working days from the date the Tax Authority receives a complete and valid dossier as prescribed. Simultaneously, update the information and change the enterprise’s TIN status to Status 03: “Taxpayer has suspended operations but has not completed procedures for termination of TIN validity” with the corresponding reason within the same working day or, at the latest, by the beginning of the next working day following the issuance of this Notice.

- Coordinate with the Tax Authority managing revenues where the enterprise has incurred obligations to the State budget to finalize the enterprise’s obligations (including full submission of tax declaration dossiers, fulfillment of tax payment and invoice obligations, and settlement of overpaid tax amounts or non-deducted value-added tax (if any)), and process tax offsetting or refunds in accordance with the law.

- Carry out procedures for offsetting or refunding-cum-offsetting regarding other obligations of the enterprise as prescribed by the Law on Tax Administration and its guiding documents.

- Request the Customs Authority to confirm that the enterprise has fulfilled its obligations for tax payments and other revenues belonging to the State budget regarding import-export activities, within 3 days from the date of issuance of the Notice of the enterprise’s suspension of operations and ongoing procedures for termination of TIN validity.

- Issue a Notice of the taxpayer’s fulfillment of tax obligations for the submission of the dissolution/termination of operations dossier to the BRO (Form No. 28/TB-DKT issued with Circular 86) within 3 working days from the date the enterprise fulfills its tax obligations with the tax management authority. Simultaneously, update the information and change the enterprise’s TIN status to Status 01: “Taxpayer has suspended operations and completed procedures for termination of TIN validity” with the corresponding reason within the same working day or, at the latest, by the beginning of the next working day following the issuance of this Notice.

Note: During the process of processing the application for termination of the enterprise’s TIN, the Tax Authority shall conduct an inspection at the enterprise’s headquarters, except for the following cases: (i) enterprises subject to Corporate Income Tax (“CIT”) calculated as a percentage of revenue from the sale of goods and services in accordance with the law on CIT; and (ii) cases where the enterprise has not incurred any revenue and has not used invoices from the time of establishment until the time of dissolution.

In practice, conducting inspections at the enterprise’s headquarters for dissolution purposes often takes a significant amount of time as such inspections fall outside the Tax Authority’s periodic inspection schedule; therefore, enterprises should take this into account to avoid affecting related plans.

2.3. Step 3: Liquidation of assets, settlement of the enterprise’s debts, and termination of TIN validity

The owner of a sole proprietorship, the Board of Members or the company owner, or the Board of Directors shall directly organize the liquidation of the enterprise’s assets, unless the company charter provides for the establishment of a separate liquidation organization[6]. The Law on Enterprises does not stipulate specific processes and procedures for the liquidation of assets upon corporate dissolution; however, the steps for conducting asset liquidation may proceed as follows:

- Competent persons of the enterprise have the task of inventorying, classifying, and quantifying assets, collecting dossiers and documents related to the assets to be liquidated, and proceeding to evaluate and determine the liquidation value and the method of liquidation for such assets.

- Upon completion of the sale of assets (if applicable), the proceeds, along with the cash available in the enterprise, shall be used to settle the debts and asset obligations of the enterprise in the following order of priority: (i) Debts related to wages, severance pay, social insurance, health insurance, and unemployment insurance in accordance with the law, and other benefits of employees under the signed collective bargaining agreement and labor contracts; (ii) Tax debts; and (iii) Other debts[7]. After the costs of corporate dissolution and all debts have been paid, the remainder shall be distributed to the owner of the sole proprietorship, members, shareholders, or the company owner in proportion to their ownership ratio of capital contributions or shares.

2.4. Step 4: Submission of the Dissolution Dossier

The legal representative of the enterprise shall submit the corporate dissolution dossier to the BRO within 5 working days from the date of full payment of the enterprise’s debts and receipt of the Notice from the Tax Authority confirming the fulfillment of tax obligations for the purpose of submitting the dissolution dossier to the BRO.

The corporate dissolution dossier includes[8]:

- Notification of corporate dissolution;

- Report on the liquidation of enterprise assets; the list of creditors and the amount of debts paid, including the full payment of tax debts and arrears of social insurance, health insurance, and unemployment insurance for employees after the decision on corporate dissolution (if any).

The dissolution dossier must be accurate and truthful. In cases where the dissolution dossier is inaccurate or fraudulent, members of the Board of Directors of a joint stock company, members of the Board of Members of a limited liability company, the company owner, the owner of a sole proprietorship, the director or general director, partnership members, and the legal representative of the enterprise shall be jointly liable for the settlement of unresolved employee benefits, unpaid taxes, and other outstanding debts, and shall be personally liable before the law for any consequences arising within a period of 5 years from the date of submission of the dossier[9].

Note: Prior to submitting the dossier for corporate dissolution registration, the enterprise must perform procedures to terminate the operations of its branches, representative offices, and business locations at the provincial-level BRO where such branches, representative offices, or business locations are situated.

2.5. Step 5: Updating the enterprise’s legal status in the National Database on Business Registration (“NDBR”)

- In case of dissolution via dossier: Upon receipt of the enterprise dissolution registration dossier, the provincial-level BRO shall send information regarding the enterprise’s registration for dissolution to the Tax Authority. Within 2 working days from the date of receipt of such information, the Tax Authority shall send its opinion on the enterprise’s fulfillment of tax obligations to the provincial-level BRO. Within 5 working days from the date of receipt of the enterprise dissolution registration dossier, the provincial-level BRO shall change the enterprise’s legal status in the NDBR to “Dissolved” if it does not receive an opinion from the Tax Authority or if it receives an opinion from the Tax Authority confirming that the enterprise has fulfilled its tax obligations; simultaneously, it shall post a notification of the enterprise’s dissolution on the NBRP. In the event the Tax Authority issues an objection because the enterprise has not fulfilled its tax obligations as prescribed, the provincial-level BRO shall issue a notice to inform the enterprise [10].

- In case of automatic dissolution: After 180 days from the date the provincial-level BRO receives the enterprise’s Dissolution Decision, if the provincial-level BRO has not received the enterprise dissolution registration dossier, the dossiers for the termination of operations of branches, representative offices, or business locations, and any written objection from the tax management authority or other related organizations or individuals, the provincial-level BRO shall change the legal status of the enterprise, branches, representative offices, and business locations in the NDBR to “Dissolved” or “Terminated”. Simultaneously, it shall issue a notice that the enterprise has been dissolved and the branches, representative offices, and business locations have terminated their operations within 03 working days from the expiration of the aforementioned period [11].

Despite the provisions on automatic dissolution as stated above, in practice, the BRO will not allow the completion of the dissolution process if the enterprise has not previously completed its tax finalization.

Note: For enterprises using seals issued by the police authority, the enterprise is responsible for returning the seal and the seal sample registration certificate to the police authority in accordance with regulations upon completion of the dissolution procedures.

[1] General Statistics Office – Ministry of Finance (2026), Report on the Socio-Economic Situation for April and the first four months of 2026, accessed at https://www.nso.gov.vn/bai-top/2026/05/bao-cao-tinh-hinh-kinh-te-xa-hoi-thang-tu-va-4-thang-dau-nam-2026/

[2] Article 211 of the Law on Enterprises.

[3] Article 14 of Circular 86.

[4] Article 14.3 of Circular 86.

[5] Article 16 of Circular 86.

[6] Article 208.2 of the Law on Enterprises.

[7] Article 208.5 of the Law on Enterprises.

[8] Article 210.1 of the Law on Enterprises.

[9] Article 210.3 of the Law on Enterprises.

[10] Article 64.5 of Decree 168.

[11] Article 64.6 of Decree 168.

Disclaimer: This article is prepared by PTN Legal LLC (“PTN Legal”) solely for the purpose of providing reference information to readers. PTN Legal does not commit to or guarantee the accuracy or completeness of this information. The content of the article may be amended, adjusted, or updated without prior notice. PTN Legal shall not be liable for any errors or omissions in this article or for any damages arising from its use in any circumstances.