A convertible loan is a financing mechanism possessing a hybrid nature between a credit transaction and an equity investment. Unlike a conventional loan, a convertible loan grants the lender the right to receive shares or a capital contribution in lieu of cash repayment upon exercising the conversion right. Such conversion may be executed at the lender’s discretion or subject to a mandatory conversion mechanism upon the satisfaction of conversion conditions, in accordance with the agreement between the parties in the loan agreement.

In practice, convertible loans are frequently utilized to finance start-ups, innovative enterprises, or growth-stage enterprises seeking to raise capital in circumstances where investors lack a sufficient basis to accurately determine the enterprise’s valuation, or do not wish to become shareholders or members of the borrowing enterprise at the time of capital disbursement. Concurrently, this mechanism still enables the lender to acquire certain governance rights or the right to access information pertaining to the borrowing enterprise.

Currently, Vietnamese law lacks specific regulations directly governing convertible loans applicable to non-listed enterprises, with the exception of the convertible bond framework applicable to joint-stock companies. Within the scope of this article, we focus on analyzing: (i) certain legal issues pertaining to convertible loans applicable to borrowing enterprises that are non-public companies in Vietnam; and (ii) the procedure for converting foreign loans into shares or capital contributions in borrowing enterprises that are non-listed companies (as illustrated in the figure below and detailed in the subsequent section).

1. Operational mechanism, advantages, and legal risks to consider

1.1. The basic operational mechanism of a convertible loan can be summarized as follows:

Firstly, the borrowing enterprise receives the loan proceeds while concurrently granting the lender the right to convert the loan into shares or a capital contribution in the borrowing enterprise. Prior to the conversion, the borrowing enterprise retains the obligation to repay the principal and interest to the lender as stipulated in the loan agreement, and the lender holds the status of a creditor to the borrowing enterprise.

Secondly, upon the occurrence of a conversion event as agreed by the parties, or when the lender elects to exercise the conversion right (subject to the transaction structure), all or a portion of the loan may be converted into shares or a capital contribution of the borrowing enterprise at a predetermined conversion ratio.

Thirdly, in the event the lender exercises the conversion right, the borrowing enterprise’s loan repayment obligation shall be substituted by the obligation to issue shares or record the corresponding capital contribution in favor of the lender. Conversely, if the conversion right is not exercised, the borrowing enterprise continues to bear the obligation to fully repay the loan, including the principal and accrued interest, in accordance with the provisions of the loan agreement.

1.2. Financing in the form of a convertible loan offers several key advantages as follows:

For the borrowing enterprise, a convertible loan enables the enterprise to raise capital without the immediate issuance of shares or capital contributions, thereby mitigating the risk of diluting the ownership interest of existing shareholders or members during the initial stage of development. Concurrently, since the lender is granted an additional right to convert the loan into shares or a capital contribution, the borrowing enterprise can often access funding at a lower interest rate compared to conventional commercial loans.

For the lender, a convertible loan creates conditions to both earn a fixed return through the loan’s interest rate and, simultaneously, secure an opportunity to participate in the enterprise’s value appreciation through the right to convert into shares or a capital contribution in the future. Prior to the conversion of the loan, the lender retains the legal status of a creditor and is entitled to payment priority over shareholders or members in the event of the enterprise’s insolvency, dissolution, or bankruptcy.

1.3. Legal risks to consider

Despite its high degree of flexibility, a convertible loan entails significant legal and financial risks for both the borrowing enterprise and the lender.

First and foremost, in terms of its legal and accounting nature, a convertible loan is still recorded as a debt obligation of the enterprise until the completion of the conversion. This may increase the financial leverage ratio and exert substantial pressure on the enterprise’s cash flow, particularly in the event the enterprise fails to successfully execute a subsequent fundraising round or no conversion event occurs prior to the maturity date. In such instances, the enterprise may be obliged to fulfill the obligation to repay the entire principal and accrued interest as committed in the loan agreement.

Furthermore, disputes arising from convertible loans in practice frequently stem from contract terms that are poorly drafted or fail to adequately provide for scenarios that may arise during the execution of the transaction. Matters such as the conversion event, maturity date, conversion price determination method, valuation cap, or anti-dilution mechanism, if not explicitly stipulated, may lead to divergent interpretations and applications between the parties, thereby heightening the risk of disputes.

2. Basic provisions of a convertible loan agreement

In practice, the parties frequently devote special attention to the following key provisions when structuring and negotiating a convertible loan transaction.

2.1. Conditions precedent to disbursement

Conditions precedent to disbursement constitute a set of conditions, documents, or events that the borrowing enterprise is strictly required to fulfill before the lender becomes obligated to disburse the loan. This provision is of paramount importance in mitigating the lender’s legal and financial risks prior to the actual transfer of funds. These conditions typically encompass the completion of the enterprise’s corporate and legal records, provision of financial statements, verification of asset ownership, obtainment of necessary internal approvals, execution of relevant transaction documents, or the assurance that no material adverse event has occurred prior to the time of disbursement. In the event the borrowing enterprise fails to satisfy or only partially satisfies the conditions precedent, the lender generally reserves the right to refuse disbursement or terminate the transaction without being deemed in breach of its contractual obligations. In practice, the scope and level of detail of the conditions precedent largely depend on the risk profile of the transaction, the financial capacity of the borrowing enterprise, and the bargaining power of the parties.

2.2. Conversion event provisions

Conversion event provisions define the circumstances that give rise to the right or obligation to convert the loan into shares or a capital contribution in the borrowing enterprise. In transaction practice, these events may include: (i) the borrowing enterprise’s business performance meeting or exceeding the designated targets; (ii) the borrowing enterprise successfully completing its prescribed organizational restructuring plan; (iii) the borrowing enterprise conducting an initial public offering (IPO); (iv) the loan reaching its maturity date; or (v) the lender exercising its optional conversion right in accordance with the agreement between the parties.

In certain instances, the agreement may also provide for a mandatory conversion mechanism upon the satisfaction of specific conditions, such as when the enterprise executes a subsequent fundraising round, the share price appreciates significantly, or the enterprise undergoes a debt restructuring. In such scenarios, the loan may be subject to mandatory conversion pursuant to the mechanism predetermined by the parties, and the lender may no longer reserve the option to maintain the loan until the maturity date.

2.3. Conversion ratio and conversion price

A convertible loan is frequently regarded as a hybrid financial instrument as it concurrently combines elements of a credit relationship and an equity investment relationship. One of the decisive components in this transaction is the mechanism for determining the conversion ratio and conversion price.

In practice, the conversion price or conversion ratio is typically determined based on the enterprise valuation at the time of conversion and may be structured as a fixed price or a pricing formula based on financial criteria previously agreed upon by the parties in the loan agreement.

The conversion ratio serves as the basis for determining the number of shares or the capital contribution that the lender will receive upon exercising the conversion right. For example, the loan agreement may stipulate that every principal debt amount valued at VND 1,000,000 can be converted into 5 ordinary shares of the borrowing enterprise.

Meanwhile, the conversion price is the price utilized to determine the number of shares the lender is entitled to receive post-conversion, which has a direct impact on the dilution level of existing shareholders’ ownership interests. For instance, if the loan value is USD 1,000,000 and the conversion price is determined at USD 5 per share, the lender shall be entitled to receive 200,000 shares upon executing the conversion.

Furthermore, market practice also observes certain high-risk conversion structures, wherein the debt is converted at a fixed monetary value, but the number of issued shares fluctuates according to the market price at the time of conversion. This mechanism may compel the enterprise to issue a substantial number of new shares, thereby causing significant dilution to the existing shareholders’ ownership percentages.

2.4. Financial covenants and material adverse effect

In convertible loan transactions, the lender frequently requires the borrowing enterprise to commit to maintaining specific financial indicators or to restrict the execution of actions that may significantly affect its solvency and enterprise valuation. These covenants may include limitations on incurring additional indebtedness, restrictions on the transfer of material assets, maintenance of a minimum working capital level, or the obligation to provide periodic financial statements.

In addition, the material adverse effect provision is typically utilized to permit the lender to suspend disbursement, demand the remedy of defaults, or enforce protective measures in the event of occurrences that severely impact the financial condition, business operations, or prospects of the borrowing enterprise.

However, during the negotiation process, the borrowing enterprise often seeks to limit the scope of application of these provisions to prevent the lender from invoking technical defaults or ordinary business fluctuations to demand early repayment or apply protective measures beyond what is strictly necessary.

2.5. The lender’s control rights and monitoring mechanisms

Although the lender does not yet hold the status of a shareholder or member of the borrowing enterprise during the pre-conversion phase, they frequently require certain monitoring rights to mitigate investment risks and track the borrowing enterprise’s operations. These rights may encompass the right to access financial information, the right to receive periodic reports, the right to attend management meetings in an observer capacity, or the right to nominate and appoint a board of directors observer.

Additionally, in certain transactions, the lender may demand the right of prior approval (or prior consent) over specific material decisions of the enterprise, such as the issuance of additional shares or capital contributions, incurring indebtedness exceeding a prescribed limit, transferring high-value assets, altering business lines, or executing related-party transactions.

In essence, these control and monitoring rights function as a mechanism to balance the interests among the parties in a context where the lender has not officially become a shareholder or member, yet still requires appropriate legal instruments to safeguard their investment against risks arising during the enterprise’s operation and development process.

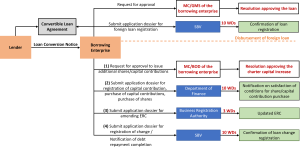

3. Procedure for converting loans into shares/capital contributions

3.1. For foreign loans

a. Loan receipt and execution phase

Prior to receiving a foreign loan, the borrowing enterprise must obtain the necessary internal approvals (from the members’ council or the general meeting of shareholders, depending on the corporate form) regarding the borrowing of funds, the receipt of the foreign loan, the mechanism for converting the loan into shares/capital contributions, and the proposed plan for increasing the charter capital post-conversion. Concurrently, the borrower must also review the foreign ownership limits applicable to conditional business lines to ensure that the loan conversion can be executed legally in accordance with investment laws.

Upon obtaining internal approvals, for medium and long-term foreign loans, the borrowing enterprise is responsible for conducting the procedure for registration of the foreign loan with the State Bank of Vietnam (“SBV“) prior to disbursement and drawdown, in compliance with foreign exchange management regulations.

In transaction practice, the aforementioned procedures are typically stipulated as conditions precedent that the borrowing enterprise must satisfy in order to obtain disbursement of the foreign loan.

b. Loan conversion phase

Step 1: Passing internal resolutions

Upon receiving the conversion notice from the lender, the borrowing enterprise must conduct internal procedures to approve the issuance of additional shares or capital contributions in compliance with the provisions of the Law on Enterprises and its Charter. The contents of such approval typically include: (i) adopting the plan to increase the charter capital; (ii) approving the issuance of shares or the receipt of the capital contribution corresponding to the value of the converted loan; and (iii) amending and supplementing the company’s charter and relevant internal governance documents to record the new ownership structure post-conversion.

Step 2: Conducting the procedure for approval of capital contribution and share purchase by foreign investors

In cases subject to the registration of capital contribution and share purchase pursuant to the Law on Investment[1], the enterprise must submit a registration dossier to the competent investment registration authority prior to executing the conversion. The investment registration authority shall review and issue a notification within 10 working days (“WDs”). Specifically, in cases where the enterprise possesses land in areas affecting national defense and security, the investment registration authority must solicit opinions from the provincial-level Military Command and Department of Public Security within a total timeframe of 10 WDs prior to issuing the notification. Only upon obtaining such approval may the enterprise proceed with the procedure to amend the enterprise registration certificate (“ERC“) at the business registration authority, as specified in Step 3 below.

Step 3: Registering changes to enterprise registration contents

Upon the completion of the partial or full conversion of the loan, the enterprise shall conduct the procedure to register changes to the ERC to record (i) the new charter capital amount; (ii) the new shareholders or members structure; and (iii) the ownership ratio of foreign investors, within 10 days from the date of such changes. Within 03 WDs from the date of receipt of the dossier, the business registration authority is responsible for examining the validity of the dossier and issuing a new ERC; in the event the dossier is invalid, the business registration authority must notify the enterprise in writing of the contents requiring amendment or supplementation. In case of refusal to issue a new ERC, it must notify the enterprise in writing and clearly state the reasons therefor[2].

Step 4: Executing procedures with the SBV regarding the foreign loan

In the case of a partial conversion of the foreign loan, the borrowing enterprise is responsible for registering the change (pertaining to the loan value) of the foreign loan with the SBV[3]. In the case of a full conversion of the foreign loan, the borrowing enterprise shall submit a written document to the SBV notifying the completion of the debt repayment obligation.

3.2. For onshore loans

For convertible loans funded by domestic lenders, the legal procedures are generally significantly simpler as there are no requirements pertaining to foreign exchange management, registration of foreign loans, or procedures for foreign investment approval. In this scenario, the conversion procedure primarily involves: (i) passing internal resolutions on the loan conversion and charter capital increase; (ii) issuing shares/capital contributions to swap the debt obligation; (iii) amending the company’s charter; and (iv) registering changes to the enterprise registration contents with the business registration authority. In practice, however, despite the absence of foreign elements, the parties must still meticulously review the internal approval authority, conversion pricing mechanism, dilution limits, and tax obligations arising from the transaction. This is of particular importance for enterprises that have undergone multiple investment rounds or involve various shareholder groups with divergent priority rights pursuant to the applicableshareholders’ agreement or company’s charter.

———-

[1] Article 21.3 of the Law on Investment No. 143/2025/QH15 of the National Assembly dated 11 December 2025, as amened from time to time.

[2] Article 30 of the Law on Enterprises No. 59/2020/QH14 of the National Assembly dated 17 June 2020, as amened from time to time .

[3] Article 17.1 of Circular No. 12/2022/TT-NHNN of the SBV dated 30 September 2022, as amended from time to time.

Disclaimer: This article has been prepared by PTN Legal Limited Liability Law Company (‘PTN Legal‘) for the sole purpose of providing reference information to readers. PTN Legal makes no representation or warranty as to the accuracy or completeness of this information. The contents of this article may be changed, amended, or updated without prior notice. PTN Legal assumes no responsibility for any errors or omissions in this article, or for any damage arising from the use of this article in any circumstances. Readers who wish to receive articles from PTN Legal by email may register their information here.

Article prepared by Ms. Dao Thi Huong Ly, Paralegal.